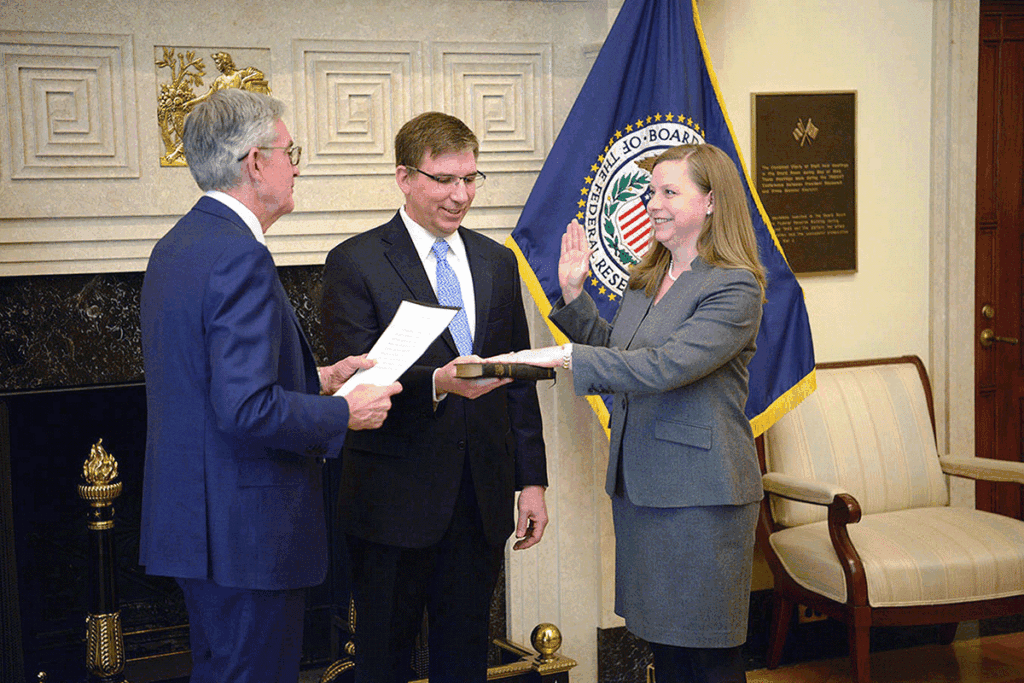

On Nov. 26, 2018, Michelle W. Bowman was appointed to the Board of Governors of the Federal Reserve System to complete an unexpired term. Reappointed in January 2020, Gov. Bowman has been sworn in for a full 14-year term that ends Jan. 31, 2034. She fills a specific role created by Congress that provides for an individual from a community banking background to serve on the Board.

Miki Bowman’s banking experience stems from her service as vice president of Farmers & Drovers Bank in Kansas from 2010 to 2017. Afterward, she served as the Kansas state bank commissioner from January 2017 to November 2018. Additional past experience, prior to banking, includes service in the Washington, D.C., office of Sen. Bob Dole of Kansas, as a counsel to the U.S. House Committee on Transportation and Infrastructure and the Committee on Government Reform and Oversight, as a director at the Federal Emergency Management Agency, and in capacity as a deputy assistant secretary and policy adviser to Homeland Security Secretary Tom Ridge.

Following her time in Washington, Bowman led a government and public affairs consultancy in London before returning to Kansas in 2010. She earned a bachelor’s degree from the University of Kansas, a JD from the Washburn University School of Law, and she is a member of the New York State Bar.

Recently, Gov. Bowman shared her insights and expertise in addressing the following questions for Hoosier Banker readers.

On the Board of Governors of the Federal Reserve System, you are the first to serve in the role created by Congress for a community banker to fill. What does your unique perspective bring to the Board?

As a former community bankers and state bank regulator, I bring the unique perspective of someone from a rural, agricultural community, who has worked to support the economic well-being of customers, businesses and their communities. My family has deep roots in rural Kansas and a long history in farming, ranching and banking. I have spent my banking career living, working and raising a family in a rural area, which aren’t typical experiences for a Fed policymaker.

I view this diversity as a strength, as Congress recognized in the creation of this role, and I believe the perspective I bring has been critical – especially during the COVID-19 pandemic. We need strong community banks because they help support strong communities and are an important economic driver for small business in America.

What are the primary responsibilities of the Board of Governors?

The Board has five key responsibilities on behalf of the American people:

- Conducting monetary policy through the Federal Open Market Committee to promote the goals of maximum employment and price stability for the U.S. economy;

- Monitoring financial system stability and seeking to minimize and contain systemic financial risk to the broader economy;

- Supervising the safety and soundness of individual financial institutions, and monitoring their impact on the broader financial system;

- Ensuring payment and settlement system safety and efficiency;

- Supporting consumer protection and community development through consumer-focused bank supervision and examination, research and analysis of emerging consumer issues and trends, community economic development activities, and the administration of consumer laws and regulations.

How has the COVID-19 pandemic affected the Board’s priorities?

Though the COVID-19 pandemic is primarily a health crisis, it caused substantial disruptions to U.S. financial markets and the economy. The Board took actions that were designed to help support households, businesses, nonprofits, and state and local governments. Guided by our dual mandate to promote maximum employment and stable prices for the American people, along with our responsibilities to promote the stability of the financial system, the Fed and the FOMC quickly:

- Lowered interest rates to near zero to bolster the economy;

- Took steps to stabilize the financial system; and

- Implemented emergency programs to support the flow of credit in the economy.

These actions helped keep many businesses and organizations from closing and better positioned employers to retain workers and to rehire as the recovery continues. The Federal Reserve also took additional actions intended to restore market functioning; support the flow of credit to households, businesses and communities; and reduce the bank regulatory reporting and compliance burden.

You have commented on the importance of bringing credit and housing opportunities to low- to moderate income communities. How can banks help with this effort?

One of the key issues related to access to credit and home ownership is often geographic proximity to a financial institution. For this reason, it is important that we have a large and diverse landscape of banks located in or near every community across the country.

Another important element of financial inclusion is financial education to empower consumers to select financial products that meet their needs while understanding what is required to maintain an account in good standing. Community banks are particularly engaged in financial education efforts with various organizations in their communities, from schools to churches to civic groups.

While progress is being made in the effort to bring more consumers into the financial system, as shown by the FDIC’s 2019 survey, How America Banks, there is still more work to be done. Approximately 5.4% – or 7.1 million of U.S. households – are unbanked. To address the problem, we need to understand who the unbanked are, and why they have chosen not to participate in and/or have left the banking system.

I am sure you are familiar with the “Bank On” program which promotes access to standardized low-cost transaction accounts for all Americans, particularly for the unbanked. To be included, an account must have the following features: $25 or less minimum deposit, free debit card, no overdraft or low balance fees, reduced monthly maintenance fees, $2.50 or less ATM fee when using out-of-network ATMs, free branch access and telephone banking, free bill pay, check cashing and monthly electronic statements. It’s innovative programs like this that help bridge the gap and bring credit and housing opportunities to low- to moderate-income communities.

You also have spoken of the Federal Reserve’s work with high schools and universities “to inspire students’ interest in economics and finance.” Please elaborate.

The Board is committed to inspiring students’ interest in pursuing education and careers in economics and finance, with an additional interest in expanding diversity. Let me share a few examples of efforts we undertake to advance this goal:

- Twice a year the Board and System host an online Federal Reserve Board event: Exploring Careers in Economics. Staff discuss career opportunities and diversity in economics and share information about career paths within the Federal Reserve System. In 2021, we partnered with The Sadie Collective to expand their membership.

- Annually, the Federal Reserve hosts the College Fed Challenge, which is a team competition for undergraduate students. This long-standing event attracted 90 teams from colleges around the country, with the final competition hosted by the Board of Governors (virtually in 2020 and 2021). Teams analyze economic and financial conditions and formulate a monetary policy recommendation, modeling the Federal Open Market Committee.

- We continue to do outreach for Exploring Careers in Economics, Fed Challenge and other economic education events to diverse universities and colleges, Historically Black Colleges and Universities (HBCUs), and Hispanic-Serving Institutions (HSIs).

- We also do considerable outreach to attract diverse candidates in our recruiting of staff. This includes participating in minority recruitment events at HBCUs, HSIs, and Hispanic professional conferences and career fairs. Our outreach is particularly notable, as we hire recent college graduates as full-time research assistants, a position which can be an important step toward a career in economics.

- The Fed also co-sponsors with the Conference of State Bank Supervisors and the FDIC the annual community bank research conference where we feature the winning undergraduate team from CSBS’ community bank case study competition. This annual competition provides students an opportunity to partner with a community bank to develop an original case study. Indiana colleges and universities have competed in the competition in most years. Several of my Federal Reserve colleagues even serve as competition judges. The winning case study is presented during the annual research conference, and the team’s research is published in CSBS’ Journal of Community Bank Case Studies. Indiana bankers interested in partnering with a student team should contact CSBS to get more information on which Indiana schools have expressed interest in the 2022 competition.

In recent months, you have often referenced optimism about economic recovery. What do you foresee for 2022 regarding the U.S. economy?

U.S. businesses and households have demonstrated great resilience as the economy continues to open, and I remain optimistic about the ongoing expansion. The economic activity reflects not just the incredible resilience of U.S. households and businesses, but also very supportive monetary and fiscal policy.

I continue to be concerned about the difficulties small businesses are experiencing around the country, particularly with employment and supply chains. I am also closely monitoring inflation pressures across the economy.

- On the price stability side of our mandate, as we have all seen, inflation has been running well above our 2% goal, and I suspect supply-and-demand imbalances are playing an important role in the rise in inflation this year. As the supply chain bottlenecks are worked out, these pressures will likely ease, but that could take some time, as some supply chain bottlenecks might continue well into 2022. And therefore, I am concerned that inflation might end up being higher than most expect. I will continue to closely monitor inflation pressures going forward.

- On the maximum employment side of our mandate, economic conditions bode well for the achievement of our goal. I expect the unemployment rate to continue to decline, but at a slightly slower rate going forward. But I am concerned about lower labor force participation and will be closely watching it. The most recent reports on employment and anecdotal reports from a wide range of businesses suggest that, even when offering higher wages and signing bonuses, many employers are finding it difficult to fill open positions. History tells us that the longer workers remain out of the workforce, the less likely it is that they will return to employment and the greater the likelihood that they will lose skills and connections with the job market, which could weigh on labor force participation for years to come. The Federal Reserve’s policy tools are useful for promoting a strong job market, but they are not well suited to addressing these harmful effects on labor supply.

What concerns you the most about the coming year that community bankers should be aware of?

As we see the economy and workforce returning to a more normal state, I would note that the banking system entered into the pandemic in a very strong financial condition, with plenty of capital and liquidity. With this in mind, community banks have continued to perform well throughout the pandemic. And I believe that community bankers will continue to provide a vital source of funding to local businesses, because they live in their communities and understand the needs and conditions of the local economy.

More generally, community banks will likely continue to face the same issues that existed prior to the pandemic, including a low interest rate environment, competition from other market participants, shifting market conditions as a result of technological innovation, and pressure to adapt and embrace technology.